Community Banking in the 21st Century

The fifth annual Community Banking in the 21st Century research and policy conference, co-sponsored by the Federal Reserve System and the Conference of State Bank Supervisors (CSBS), took place October 4-5 at the Federal Reserve Bank of St. Louis. The conference brought together community bankers, academics, policymakers and bank regulators to discuss the latest research on community banking.

The conference presents an innovative approach to the study of community banks. Academics explore issues raised by the industry in a neutral, empirical manner and present their findings at the conference. Community bankers contribute to an annual national survey prior to the conference and then participate directly in the conference by serving as keynote speakers and panelists and by providing feedback to the research presented.

This year’s guest speakers included Federal Reserve Chair Janet Yellen; CSBS Chairman and Wyoming Division of Banking Commissioner Albert Forkner; and CSBS President and CEO John Ryan. Keynote speakers include Cynthia Blankenship, vice chairman, corporate president and chief financial officer of Grapevine, Texas-based Bank of the West; and Federal Reserve Bank of San Francisco President John Williams.

The call for papers for this year's conference opened Feb. 2, 2017.

For more information, please contact conference@communitybanking.org.

Conference Agenda

Gateway Auditorium, 6th Floor | Federal Reserve Bank of St. Louis

October 4-5, 2017

Download as PDF

- Wednesday, October 4

-

Arrival and Networking

-

Welcoming Remarks

Albert Forkner

Albert Forkner

State Banking Commissioner, Wyoming Division of Banking; Chairman, Conference of State Bank Supervisors - CSBS

-

Opening Remarks

-

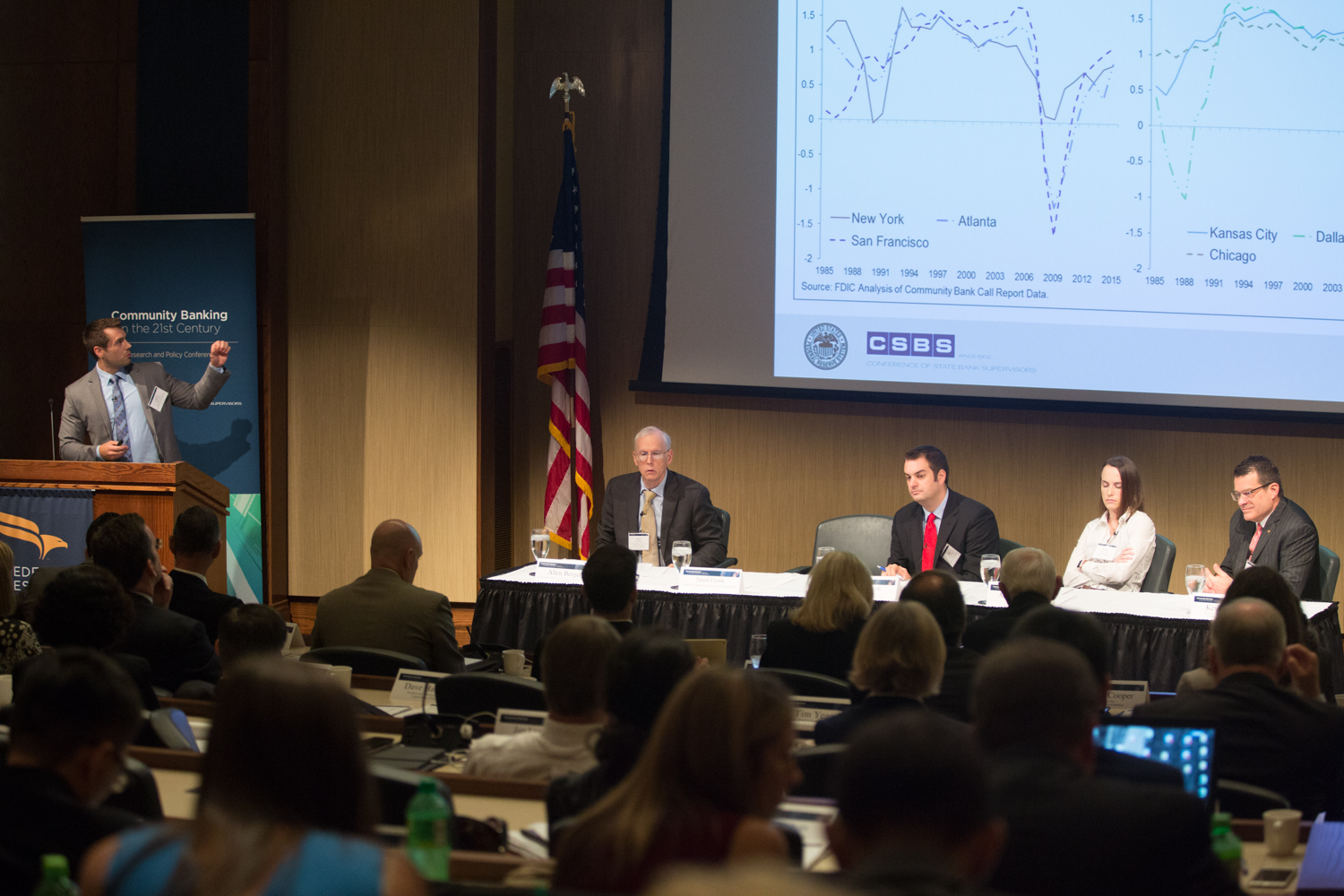

Research Paper Session 1

Supervision, Regulation and Bank Risk Moderator: Robert DeYoung

Moderator: Robert DeYoung

Capitol Federal Distinguished Professor in Financial Markets and Institutions, University of Kansas

Community Bank Discussant: Martin Birmingham

Community Bank Discussant: Martin Birmingham

President and Chief Executive Officer, Five Star Bank, Rochester, N.Y.

The Effect of Bank Supervision on Risk-Taking: Evidence from a Natural ExperimentJohn Kandrac, Board of Governors of the Federal Reserve SystemDoes Bank Supervision Matter? Evidence from Regulatory Office ClosuresJens Hagendorff, University of EdinburghRules and Judgment in the Oversight of Bank Accounting PracticesMichelle Neely, Federal Reserve Bank of St LouisRisk-insensitive RegulationAlexander Bleck, Sauder School of Business at the University of British ColumbiaReaction to the Supervision, Regulation and Bank Risk Session: Robert DeYoung and Martin BirminghamSupervision, Regulation and Bank Risk Session: Moderated Q&A -

Break

-

Presentation of Winning Case Study and Video from the 2017 CSBS Community Bank Case Study Competition

University of Akron Introduction: Charlotte Corley

Introduction: Charlotte Corley

Commissioner, Mississippi Department of Banking and Consumer Finance; chairman, Conference of State Bank Supervisors - CSBS

Case Study TeamJeffrey Kelbach, Michael Moore, Jacob Ruocchio-Cole and Kenan Sprague, University of Akron

Faculty AdvisorBhanu Balasubramnian, Associate Professor of Finance, University of Akron

Community Bank PartnerChuck Sulerzyski, President and Chief Executive Officer, Peoples Bank, Marietta, Ohio

Moderated Q&A -

Evening Reception and DinnerHyatt Regency St. Louis at the Arch

-

Evening Keynote Address

Cynthia Blankenship

Cynthia Blankenship

Vice Chairman, Corporate President and Chief Financial Officer, Bank of the West, Grapevine, Texas

Hyatt Regency St. Louis at the Arch - Thursday, October 5

-

Breakfast and Networking

-

Morning Keynote Address

-

Research Paper Session 2

Factors Influencing Bank Behavior and Performance Moderator: Allen Berger

Moderator: Allen Berger

H. Montague Osteen, Jr., Professor of Banking and Finance, Darla Moore School of Business, University of South Carolina

Community Bank Discussant: Kevin Riley

Community Bank Discussant: Kevin Riley

President and Chief Executive Officer, First Interstate Bank, Billings, Mont.

Core Profitability of Community Banks, 1985-2015Jared Fronk, Federal Deposit Insurance Corporation (FDIC)Competition and Bank FragilityW. Blake Marsh, Federal Reserve Bank of Kansas CityRegulatory Asset Thresholds and Acquisition Activity in the Banking IndustryAllison Nicoletti, Wharton School of the University of PennsylvaniaReaction to the Factors Influencing Bank Behavior and Performance Session: Kevin Riley and Allen BergerFactors Influencing Bank Behavior and Performance Session: Moderated Q&A -

Break

-

Research Paper Session 3

Real Effects of Government Policies Moderator: Timothy Yeager

Moderator: Timothy Yeager

Arkansas Bankers Association Chair in Banking at the Sam M. Walton College of Business, University of Arkansas

Community Bank Discussant: Peter Schork

Community Bank Discussant: Peter Schork

Co-founder, President and Chief Executive Officer, Ann Arbor State Bank, Ann Arbor, Mich.

Financial Crises and Filling the Credit Gap: The Role of Government-guaranteed LoansJohn Hackney, University of ArkansasThe Real Effects of Geographic Lending Disclosure on BanksYiwei Dou, New York UniversityColor and Credit: Race, Regulation and the Quality of Financial ServicesTaylor Begley, Washington University in St. LouisReaction to the Real Effects of Government Policies Session: Peter Schork and Tim YeagerReal Effects of Government Policies Session: Moderated Q&A -

Lunch

-

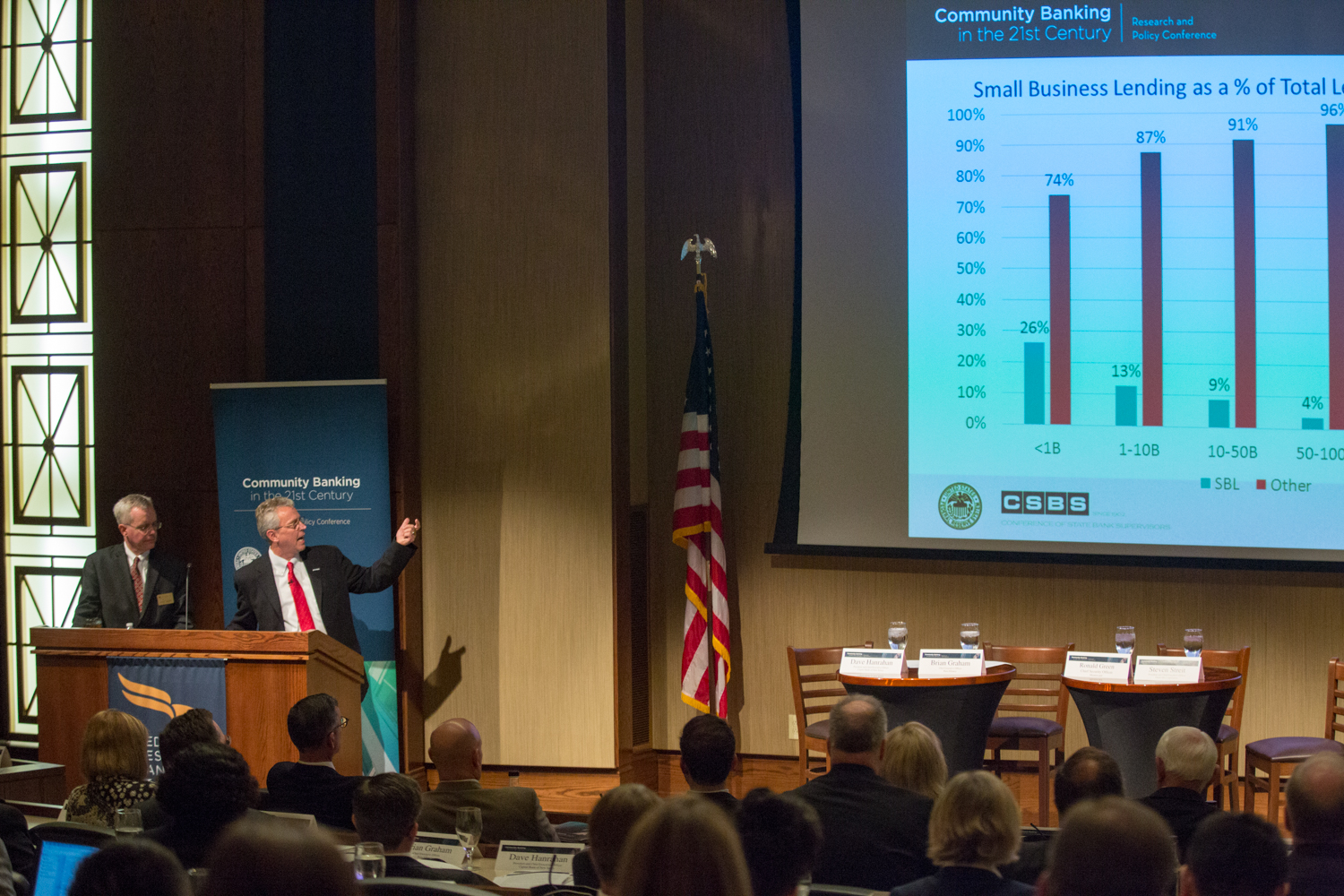

2017 National Survey of Community Banks

Presentation of Results2017 National Survey Chart Book2017 National Survey Chart Book -

Panel Discussion: Community Banking in the 21st Century: 2017 National Survey of Community Banks and State Roundtables

Moderator: David Hanrahan

Moderator: David Hanrahan

President and Chief Executive Officer, Capital Bank of New Jersey, Vineland, N.J.

Panelists Ron Green

Ron Green

Chief Information Security Officer and Group Executive, Mastercard Operation & Technology / Law Franchise Integrity

Panel Discussion -

Conference Adjourns

Research Papers, Authors and Key Findings

Research Paper Session 1

Supervision, Regulation and Bank Risk

The Effect of Bank Supervision on Risk Taking: Evidence from a Natural Experiment

Authors: John Kandrac, Board of Governors of the Federal Reserve System; Bernd Schlusche, Board of Governors of the Federal Reserve System

Key Findings: In the early 1980s, the vast majority of supervisory employees in the Ninth District of The Federal Home Loan Bank (FHLB), operating out of Little Rock, Arkansas, quit rather than relocate to Dallas, Texas. The authors use this event to study the effects of a reduction in supervisory attention. They find that the affected thrifts increased risky real estate investments and experienced higher-cost failures, relative to thrifts in other districts. They conclude that banking supervision is a vital element of banking policy that has important effects on bank behavior and protects taxpayers from costly failures.

Does Bank Supervision Matter? Evidence from Regulatory Office Closures

Authors: Jens Hagendorff, University of Edinburgh; Ivan Lim, Leeds University; Seth Armitage, University of Edinburgh

Key Findings: The authors use the closure of 11 regional offices of Federal bank regulatory agencies, 1984 to 2013, to study “negative shocks to the efficacy of supervision.” They hypothesize that a shift in the location of oversight from a local (closed) regulatory office to a more distant office increases the costs for examiners to collect and verify bank specific information. They find that banks affected by office closures, relative to unaffected banks operating within the same geographic markets, lend more and are riskier, less profitable and more likely to fail. They conclude, first, that the organizational structure of supervisors is important and, second, that its effectiveness can be can be linked to informational capabilities.

Rules and Judgment in the Oversight of Bank Accounting Practices

Authors: Michelle Neely, Federal Reserve Bank of St Louis; Drew Dahl, Federal Reserve Bank of St Louis; Andrew Meyer, Federal Reserve Bank of St. Louis

Key Findings: The authors analyze how banks of different size adhere to ostensibly “one size fits all” accounting guidelines prescribing that provisions for loan losses anticipate subsequent charge-offs. They find that correlations of provisions and charge-offs are lesser for smaller banks, which they interpret as consistent with a hypothesis that bank regulators are able to reconcile rules and judgment by “tailoring” their supervisory practices to the unique characteristics of community banks. They also find that the exercise of judgment may be associated with greater lending as well as with a greater vulnerability to potential failure.

Risk-insensitive Regulation

Author: Alexander Bleck, Sauder School of Business at the University of British Columbia

Key Findings: This article is a theoretical paper describing how, when a bank has an informational advantage over a bank regulator, it leads to a trade-off: relying on information from banks to refine regulation improves bank risk-taking but also aggravates systemic risk in the banking system and undermines its informativeness. The model explains why the observed relationship between measured risk and actual risk is low. It also shows that when market frictions (information asymmetry and the cost of systemic risk) become more severe, optimal regulation becomes more risk-insensitive.

Reaction to the Supervision, Regulation and Bank Risk Session: Robert DeYoung and Martin Birmingham

Supervision, Regulation and Bank Risk Session: Moderated Q&A

Research Paper Session 2

Factors Influencing Bank Behavior and Performance

Core Profitability of Community Banks, 1985-2015

Author: Jared Fronk, Federal Deposit Insurance Corporation (FDIC)

Key Findings: The author finds that the “core” profitability of community banks has been relatively stable across the thirty-year period ending in 2015. From this perspective, observed declines in returns on assets following the recent financial crisis—which sometimes have been described as dire—are “largely attributable” to the severity of the downturn in macroeconomic factors. He concludes that the fundamental earnings model of community banks remains sound.

Competition and Bank Fragility

Authors: W. Blake Marsh, Federal Reserve Bank of Kansas City; Rajdeep Sengupta, Federal Reserve Bank of Kansas City

Key Findings: The authors find that community banks increase commercial real estate loan holdings, and decrease shares of residential real estate mortgages and consumer loans held, following entry into their markets of larger bank competitors. This is consistent with theories that suggest that, following entry of large banks, community banks lose market share in low-risk, transactions-based retail lending but leverage their knowledge of the local market to focus on relatively riskier activities.

Regulatory Asset Thresholds and Acquisition Activity in the Banking Industry

Authors: Allison Nicoletti, Wharton School of the University of Pennsylvania ; Hailey Ballew, The Ohio State University; Michael Iselin, University of Minnesota

Key Findings: The authors test a hypothesis that compliance costs imposed on banks with assets greater than $10 billion, under the Dodd-Frank Wall Street Reform and Consumer Protection Act, increase the demand for acquisition activity approaching and just above this threshold. Their empirical evidence leads to a conclusion that implementing regulations on the basis of asset thresholds can contribute to consolidation in the banking industry.

Reaction to the Factors Influencing Bank Behavior and Performance Session: Kevin Riley and Allen Berger

Factors Influencing Bank Behavior and Performance Session: Moderated Q&A

Research Paper Session 3

Real Effects of Government Policies

Financial Crises and Filling the Credit Gap: The Role of Government-guaranteed Loans

Author: John Hackney, University of Arkansas

Key Findings: The author analyzes the impact of government guarantees on small business lending during the recent financial crisis, during which impacts of financial constraints in private credit markets were pronounced. He finds evidence that, within a given geographic market, the number of bank branches offering loans guaranteed by the Small Business Administration is positively associated with market growth in small business loans. This growth, moreover, increases employment at the smallest firms but does not increase defaults on loans.

The Real Effects of Geographic Lending Disclosure on Banks

Authors: Yiwei Dou, New York University; Youli Zou, George Washington University

Key Findings: Community organizations leverage access to the geographical distribution of loans mandated by the Community Reinvestment Act (CRA) to press for lending under its requirement that banks meet local credit needs. The authors examine the 2005 exemption of this disclosure mandate and find that banks that take the exemption, relative to those that do not, experience a reduction in non-performing loans. They conclude that mandatory disclosure for some banks results in a “deterioration” of loan underwriting quality.

Color and Credit: Race, Regulation and the Quality of Financial Services

Authors: Taylor Begley, Washington University in St. Louis; Amiyatosh Purnanandam, Ross School of Business, University of Michigan

Key Findings: The authors find that the quality of services provided to bank customers is lower in markets with lower incomes and higher minority populations. They also find that requirements under the Community Reinvestment Act to increase the quantity of services have an unintended consequence of lowering the quality of services delivered, which is consistent with incentives for banks to dilute quality when quantity is regulated.

Reaction to the Real Effects of Government Policies Session: Peter Schork and Tim Yeager

Real Effects of Government Policies Session: Moderated Q&A

Speakers and Panelists

Taylor Begley is an assistant professor of finance at the Olin Business School at Washington University in St. Louis. His research interests include financial intermediation, financial regulation and housing markets. His recent research uncovers unintended consequences of various financial regulations and government lending programs, including those that exacerbate existing racial disparities in credit access. His work has been published in the Review of Financial Studies and the Journal of Financial Economics. Begley holds a Bachelor of Science and a Master of Science in electrical engineering from the University of Kentucky and earned his Ph.D. in finance at the University of Michigan.

Allen N. Berger is the H. Montague Osteen, Jr., Professor in Banking and Finance and Ph.D. coordinator of the Finance Department, Darla Moore School of Business; Carolina Distinguished Professor, University of South Carolina; senior fellow, Wharton Financial Institutions Center; and fellow, European Banking Center. He also serves on the editorial boards of six professional finance journals. In addition, Berger is past editor of the Journal of Money, Credit, and Banking from 1994-2001 and has co-edited six special issues of various professional journals and the first and second editions of the Oxford Handbook of Banking, and will be co-editing the third edition, due out in 2020. His research covers a variety of topics related to financial institutions. He is co-author of Bank Liquidity Creation and Financial Crises (2016, Elsevier) and will be co-author of TARP and other Bank Bailouts and Bail-Ins around the World: Connecting Wall Street, Main Street, and the Financial System, due out in 2019. He has published more than 100 professional articles in refereed journals, including papers in top finance journals, Journal of Finance, Journal of Financial Economics, Review of Financial Studies, Journal of Financial and Quantitative Analysis, Review of Finance, and Journal of Financial Intermediation; top economics journals, Journal of Political Economy, American Economic Review, Review of Economics and Statistics, and Journal of Monetary Economics; and other top professional business journals, Management Science and Journal of Business; and more than 30 other non-refereed publications. His research has been cited more than 50,000 times according to Google Scholar. Berger was named professor of the year for 2015-2016 by the Darla Moore School of Business Doctoral Students Association. He was also secretary/treasurer, Financial Intermediation Research Society from 2008-2016; and senior economist from 1989 to 2008 and economist from 1982-1989 at the Board of Governors of the Federal Reserve System. He received a Ph.D. in economics from the University of California at Berkeley in 1983, and a bachelor’s degree in economics from Northwestern University in 1976.

Allen N. Berger is the H. Montague Osteen, Jr., Professor in Banking and Finance and Ph.D. coordinator of the Finance Department, Darla Moore School of Business; Carolina Distinguished Professor, University of South Carolina; senior fellow, Wharton Financial Institutions Center; and fellow, European Banking Center. He also serves on the editorial boards of six professional finance journals. In addition, Berger is past editor of the Journal of Money, Credit, and Banking from 1994-2001 and has co-edited six special issues of various professional journals and the first and second editions of the Oxford Handbook of Banking, and will be co-editing the third edition, due out in 2020. His research covers a variety of topics related to financial institutions. He is co-author of Bank Liquidity Creation and Financial Crises (2016, Elsevier) and will be co-author of TARP and other Bank Bailouts and Bail-Ins around the World: Connecting Wall Street, Main Street, and the Financial System, due out in 2019. He has published more than 100 professional articles in refereed journals, including papers in top finance journals, Journal of Finance, Journal of Financial Economics, Review of Financial Studies, Journal of Financial and Quantitative Analysis, Review of Finance, and Journal of Financial Intermediation; top economics journals, Journal of Political Economy, American Economic Review, Review of Economics and Statistics, and Journal of Monetary Economics; and other top professional business journals, Management Science and Journal of Business; and more than 30 other non-refereed publications. His research has been cited more than 50,000 times according to Google Scholar. Berger was named professor of the year for 2015-2016 by the Darla Moore School of Business Doctoral Students Association. He was also secretary/treasurer, Financial Intermediation Research Society from 2008-2016; and senior economist from 1989 to 2008 and economist from 1982-1989 at the Board of Governors of the Federal Reserve System. He received a Ph.D. in economics from the University of California at Berkeley in 1983, and a bachelor’s degree in economics from Northwestern University in 1976.

Martin K. Birmingham has been the president and chief executive officer of Financial Institutions, Inc., and Five Star Bank since 2013. He served as president and chief of community banking at Five Star Bank in 2012 and 2013 and as senior vice president, commercial banking executive and Rochester region president from 2005 to 2012. He was promoted to executive vice president in 2009. He was president and CEO of the National Bank of Geneva, a wholly owned subsidiary of the company, in 2005. Previously he served in progressive corporate banking roles at Fleet Boston Financial Group/Bank of America including as regional president. Birmingham serves on several not-for-profit boards including: AAA of Central and Western New York (past chair), the Greater Rochester Chamber of Commerce, University of Rochester Medical Center, St. John Fisher College (chairman), Monroe Community College Foundation, and the New York Bankers Association (chairman of the Profit Solutions committee). He is also a member of the Federal Reserve Bank of New York’s Community Depository Institutions Advisory Council. Birmingham earned his bachelor’s degree in economics from St. Lawrence University and his Master of Business Administration degree from Simon Business School at the University of Rochester.

Martin K. Birmingham has been the president and chief executive officer of Financial Institutions, Inc., and Five Star Bank since 2013. He served as president and chief of community banking at Five Star Bank in 2012 and 2013 and as senior vice president, commercial banking executive and Rochester region president from 2005 to 2012. He was promoted to executive vice president in 2009. He was president and CEO of the National Bank of Geneva, a wholly owned subsidiary of the company, in 2005. Previously he served in progressive corporate banking roles at Fleet Boston Financial Group/Bank of America including as regional president. Birmingham serves on several not-for-profit boards including: AAA of Central and Western New York (past chair), the Greater Rochester Chamber of Commerce, University of Rochester Medical Center, St. John Fisher College (chairman), Monroe Community College Foundation, and the New York Bankers Association (chairman of the Profit Solutions committee). He is also a member of the Federal Reserve Bank of New York’s Community Depository Institutions Advisory Council. Birmingham earned his bachelor’s degree in economics from St. Lawrence University and his Master of Business Administration degree from Simon Business School at the University of Rochester.

Cynthia L. Blankenship is vice chairman, corporate president and chief financial officer of Bank of the West, Grapevine, Texas. Bank of the West specializes in small business lending and has eight locations in Texas. She is currently a member of the board of directors for the Independent Community Bankers of America (ICBA). She is a past chairman of the ICBA and is the immediate past chair of the ICBA services network. Blankenship has also served on the Federal Deposit Insurance Corporation’s Community Banking Advisory Board. She was appointed Dean for Bankers and chaired the Southwestern School of Banking Foundation at Southern Methodist University from 2006 to 2009. In 2009, she received the Distinguished Alumni Award from the Southwestern Graduate School of Banking, Southern Methodist University Cox School of Business. Blankenship served as chair of the Independent Bankers Association of Texas (IBAT) in 2002 and served as chair of the IBAT Education Foundation which raised more than $1 million for financial literacy. In 2004, U.S. Banker magazine named her one of the 50 Most Powerful Women in Banking. Blankenship has served her community through the Colleyville Women’s Club, the Community Bankers Education Foundation, the Bear Creek Community Development Project, and Dallas Summer Musicals. She is a member of the Grapevine Chamber of Commerce and a recipient of the 1999 Arts Education Award and the 2004 Colleyville Women’s Club Novus Award. Blankenship currently sits on the board of directors of the Grapevine, Texas, Convention and Visitors Bureau. In November 2010, she was named as one of the 2010 Great Women of Texas.

Alexander Bleck is an assistant professor of accounting at the Sauder School of Business at the University of British Columbia. He was previously on the faculty of the University of Chicago's Booth School of Business. His research highlights limits of using the market for information to improve the firm, set accounting standards, design bank regulation, conduct monetary policy, and allocate resources in financial markets. His work has been published in the Journal of Accounting Research and the Journal of Monetary Economics. Bleck presented his work at various policy institutions including the Federal Reserve Banks of Atlanta, Chicago, Cleveland, Philadelphia, and Richmond, the Bank for International Settlements, the Bank of Canada, and the International Monetary Fund. He holds a Ph.D. in finance from the London School of Economics.

Alexander Bleck is an assistant professor of accounting at the Sauder School of Business at the University of British Columbia. He was previously on the faculty of the University of Chicago's Booth School of Business. His research highlights limits of using the market for information to improve the firm, set accounting standards, design bank regulation, conduct monetary policy, and allocate resources in financial markets. His work has been published in the Journal of Accounting Research and the Journal of Monetary Economics. Bleck presented his work at various policy institutions including the Federal Reserve Banks of Atlanta, Chicago, Cleveland, Philadelphia, and Richmond, the Bank for International Settlements, the Bank of Canada, and the International Monetary Fund. He holds a Ph.D. in finance from the London School of Economics.

Charlotte Corley is the commissioner of the Mississippi Department of Banking and Consumer Finance (DBCF). She was appointed in November 2014. After joining the DBCF in 1985 as a bank examiner, Corley worked her way through the ranks to become banking division director in 2000 and deputy commissioner in 2013. A native Mississippian, Corley earned her Bachelor of Business Administration in banking and finance from Mississippi State University. She is a graduate of the School of Banking of the South at Louisiana State University, as well as the American Bankers Association’s National Graduate Trust School at Northwestern University. She is chairman of the Conference of State Bank Supervisors (CSBS), the nation’s leading advocate for the state banking system and the only national organization dedicated to advancing the state banking system. She was a longstanding member of the Interagency Supervisory Processes Committee, helping coordinate the processes of federal and state banking regulatory agencies. She is a past member of CSBS’s state supervisory processes and technology committees and is the former chair of its education foundation. Corley has also served as a member of the Federal Financial Institutions Examination Council’s Task Force on examiner education.

Charlotte Corley is the commissioner of the Mississippi Department of Banking and Consumer Finance (DBCF). She was appointed in November 2014. After joining the DBCF in 1985 as a bank examiner, Corley worked her way through the ranks to become banking division director in 2000 and deputy commissioner in 2013. A native Mississippian, Corley earned her Bachelor of Business Administration in banking and finance from Mississippi State University. She is a graduate of the School of Banking of the South at Louisiana State University, as well as the American Bankers Association’s National Graduate Trust School at Northwestern University. She is chairman of the Conference of State Bank Supervisors (CSBS), the nation’s leading advocate for the state banking system and the only national organization dedicated to advancing the state banking system. She was a longstanding member of the Interagency Supervisory Processes Committee, helping coordinate the processes of federal and state banking regulatory agencies. She is a past member of CSBS’s state supervisory processes and technology committees and is the former chair of its education foundation. Corley has also served as a member of the Federal Financial Institutions Examination Council’s Task Force on examiner education.

Robert (Bob) DeYoung is the Capitol Federal Distinguished Professor in Financial Markets and Institutions, and Harold Otto Professor of Economics, at the University of Kansas (KU) School of Business. He is also co-editor of the Journal of Money, Credit and Banking. Prior to his academic career, DeYoung spent 15 years in the research groups of the Office of the Comptroller of the Currency, the Federal Reserve Bank of Chicago, and the Federal Deposit Insurance Corporation. DeYoung has written extensively on the performance and regulation of financial institutions in leading academic journals, regulatory publications and the financial press. He earned a bachelor’s degree from Rutgers University-Camden in 1983 and a doctorate in economics from the University of Wisconsin-Madison in 1989.

Robert (Bob) DeYoung is the Capitol Federal Distinguished Professor in Financial Markets and Institutions, and Harold Otto Professor of Economics, at the University of Kansas (KU) School of Business. He is also co-editor of the Journal of Money, Credit and Banking. Prior to his academic career, DeYoung spent 15 years in the research groups of the Office of the Comptroller of the Currency, the Federal Reserve Bank of Chicago, and the Federal Deposit Insurance Corporation. DeYoung has written extensively on the performance and regulation of financial institutions in leading academic journals, regulatory publications and the financial press. He earned a bachelor’s degree from Rutgers University-Camden in 1983 and a doctorate in economics from the University of Wisconsin-Madison in 1989.

Yiwei Dou is an assistant professor of accounting at the New York University Stern School of Business, where he teaches financial accounting to undergraduate and Master of Business Administration students. His research focuses on causes and consequences of financial reporting decisions, with a special interest in accounting and disclosure practices of financial institutions. His work has been published in leading academic journals including The Accounting Review and Journal of Accounting & Economics. Dou holds a Ph.D. from the University of Toronto Rotman School of Management, a master’s degree in economics from York University, Canada, and a bachelor’s degree in accounting from Peking University, China.

Yiwei Dou is an assistant professor of accounting at the New York University Stern School of Business, where he teaches financial accounting to undergraduate and Master of Business Administration students. His research focuses on causes and consequences of financial reporting decisions, with a special interest in accounting and disclosure practices of financial institutions. His work has been published in leading academic journals including The Accounting Review and Journal of Accounting & Economics. Dou holds a Ph.D. from the University of Toronto Rotman School of Management, a master’s degree in economics from York University, Canada, and a bachelor’s degree in accounting from Peking University, China.

Albert Forkner was selected by the Wyoming Director of the Department of Audit to head the Wyoming Division of Banking as state banking commissioner in April 2012. In this role, Forkner is responsible for the supervision and regulation of all state-chartered banks, independent trust companies, and licensed non-depository financial entities operating in Wyoming. Forkner has more than 18 years with the Wyoming Division of Banking. Prior to serving as commissioner, Forkner was the assistant banking commissioner at the division, a position he held for four years. His experience also includes senior bank examiner and chief examiner at the division, and as a commercial and real estate loan officer. Forkner received a bachelor’s degree in economics from the University of Wyoming and is a graduate of the Cannon Financial Institute and the Graduate School of Banking at the University of Colorado.

Albert Forkner was selected by the Wyoming Director of the Department of Audit to head the Wyoming Division of Banking as state banking commissioner in April 2012. In this role, Forkner is responsible for the supervision and regulation of all state-chartered banks, independent trust companies, and licensed non-depository financial entities operating in Wyoming. Forkner has more than 18 years with the Wyoming Division of Banking. Prior to serving as commissioner, Forkner was the assistant banking commissioner at the division, a position he held for four years. His experience also includes senior bank examiner and chief examiner at the division, and as a commercial and real estate loan officer. Forkner received a bachelor’s degree in economics from the University of Wyoming and is a graduate of the Cannon Financial Institute and the Graduate School of Banking at the University of Colorado.

Jared Fronk is a senior financial economist in the Economic Risk Analysis group at the Federal Deposit Insurance Corporation. Prior to his time at the FDIC, Fronk worked at the U.S. International Trade Commission and at the World Bank. He graduated magna cum laude with a degree in international relations from Brigham Young University in 2008. He received his Ph.D. in economics from Georgetown University in 2015 for his dissertation entitled “Essays on International Agreements on Government Procurement.”

Jared Fronk is a senior financial economist in the Economic Risk Analysis group at the Federal Deposit Insurance Corporation. Prior to his time at the FDIC, Fronk worked at the U.S. International Trade Commission and at the World Bank. He graduated magna cum laude with a degree in international relations from Brigham Young University in 2008. He received his Ph.D. in economics from Georgetown University in 2015 for his dissertation entitled “Essays on International Agreements on Government Procurement.”

Brian Graham is the chief executive officer of BancAlliance. BancAlliance is a network of more than 200 community banks that capitalizes on its collective scale to empower member banks to be successful in markets that have become dominated by the largest banks in the country. Previously, Graham held various leadership positions in financial services including at a private investment firm, a commercial banking company, Fannie Mae and Morgan Stanley. Brian has also served in government, both as the financial services aide to then-Congressman Charles Schumer during the thrift crisis of the 1980s and as a staff member on the “Brady Commission” which investigated the causes of the 1987 stock market crash.

Brian Graham is the chief executive officer of BancAlliance. BancAlliance is a network of more than 200 community banks that capitalizes on its collective scale to empower member banks to be successful in markets that have become dominated by the largest banks in the country. Previously, Graham held various leadership positions in financial services including at a private investment firm, a commercial banking company, Fannie Mae and Morgan Stanley. Brian has also served in government, both as the financial services aide to then-Congressman Charles Schumer during the thrift crisis of the 1980s and as a staff member on the “Brady Commission” which investigated the causes of the 1987 stock market crash.

Ron Green is the chief security officer at Mastercard. He leads a global team that ensures the safety and security of the Mastercard network as well as internal and external products and services. He is responsible for information security operations, architecture and engineering, security event management and incident response. Green also oversees cryptographic key management, business continuity, disaster recovery and emergency management. Green joined Mastercard in 2014 after serving as deputy chief information security officer at Fidelity Information Services (FIS). Prior to this position, he was director, Investigation and Protections Operations at Blackberry, and before that, as a senior vice president across several areas at Bank of America. Green has extensive experience working with international and federal law enforcement agencies both as a special agent in the United States Secret Service and as an officer in the United States Army. He was one of the first agents to receive formal training on seizing and analyzing electronic evidence, and worked on a number of international cyber-crime investigations. Green serves on the Financial Services/ Information Sharing and Analysis Center and the Overseas Security Advisory Council. He holds a bachelor’s degree in mechanical engineering from the United States Military Academy at West Point; is a graduate of the Federal Bureau of Investigation’s Domestic Security Executive Academy; and holds a graduate certification in information assurance from George Washington University.

Ron Green is the chief security officer at Mastercard. He leads a global team that ensures the safety and security of the Mastercard network as well as internal and external products and services. He is responsible for information security operations, architecture and engineering, security event management and incident response. Green also oversees cryptographic key management, business continuity, disaster recovery and emergency management. Green joined Mastercard in 2014 after serving as deputy chief information security officer at Fidelity Information Services (FIS). Prior to this position, he was director, Investigation and Protections Operations at Blackberry, and before that, as a senior vice president across several areas at Bank of America. Green has extensive experience working with international and federal law enforcement agencies both as a special agent in the United States Secret Service and as an officer in the United States Army. He was one of the first agents to receive formal training on seizing and analyzing electronic evidence, and worked on a number of international cyber-crime investigations. Green serves on the Financial Services/ Information Sharing and Analysis Center and the Overseas Security Advisory Council. He holds a bachelor’s degree in mechanical engineering from the United States Military Academy at West Point; is a graduate of the Federal Bureau of Investigation’s Domestic Security Executive Academy; and holds a graduate certification in information assurance from George Washington University.

John Hackney is an Assistant Professor of Finance at the Walton College of Business, University of Arkansas. He previously held the position of Assistant Professor of Finance at the Darla Moore School of Business, University of South Carolina. He has served on the program committee for the Community Banking Research Conference, and received the Most Important Contribution to Banking Policy Award at the 2019 Conference. His research focuses on entrepreneurship, FinTech, household finance, empirical corporate finance, and banking. John has a BA in Economics and Finance from Gonzaga University, and a MS and PhD in Finance and Business Economics from the University of Washington.

Jens Hagendorff is professor of finance at the University of Edinburgh in Scotland (UK). Prior to that, he was professor of finance and investment at Cardiff University, the AmBank Financial Services Professor at the University of Malaya (Malaysia), and the Martin Currie Professor in Finance and Investment at the University of Edinburgh. Hagendorff previously worked at the financial stability department of the Bank of Spain and as a lecturer at the University of Leeds (UK). His main area of research focuses on the intersection between corporate governance, risk and regulation in banks. He has a doctorate in economics and a Ph.D. in finance from the University of Leeds.

Jens Hagendorff is professor of finance at the University of Edinburgh in Scotland (UK). Prior to that, he was professor of finance and investment at Cardiff University, the AmBank Financial Services Professor at the University of Malaya (Malaysia), and the Martin Currie Professor in Finance and Investment at the University of Edinburgh. Hagendorff previously worked at the financial stability department of the Bank of Spain and as a lecturer at the University of Leeds (UK). His main area of research focuses on the intersection between corporate governance, risk and regulation in banks. He has a doctorate in economics and a Ph.D. in finance from the University of Leeds.

David J. Hanrahan, Sr., is the founding president and chief executive officer of Capital Bank of New Jersey. Prior to 2006, he spent 16 years at the Bank of Gloucester County, now part of Fulton Bank of New Jersey. Hanrahan holds a bachelor’s degree in accounting from Rutgers University - Camden School of Business. He is also a graduate of the American Bankers Association’s Stonier Graduate School of Banking. In 2010, he was recognized by the New Jersey Bankers Association as a new leader in banking. In 2013, he received a professionally accomplished alumni award from Rutgers University – Camden School of Business, and in that year he was also named an executive of the year by South Jersey Biz magazine. Hanrahan is a member of the Federal Reserve Bank of Philadelphia’s Community Depository Institutions Advisory Council. He is a director of the American Bankers Association (ABA) Foundation, is a past chairman of the ABA’s community and economic development committee, and is a past member of the ABA’s Community Bankers Council. He serves on the board of directors of Atlantic Community Bankers Bank. He also serves as a member of the Rutgers University - Camden School of Business Dean’s Leadership Council. From 2008 to 2015, he was a director and past board president of Cumberland County Habitat for Humanity. He is also a member of the Vineland Rotary Club and of Tenth Presbyterian Church in Philadelphia, Penn.

David J. Hanrahan, Sr., is the founding president and chief executive officer of Capital Bank of New Jersey. Prior to 2006, he spent 16 years at the Bank of Gloucester County, now part of Fulton Bank of New Jersey. Hanrahan holds a bachelor’s degree in accounting from Rutgers University - Camden School of Business. He is also a graduate of the American Bankers Association’s Stonier Graduate School of Banking. In 2010, he was recognized by the New Jersey Bankers Association as a new leader in banking. In 2013, he received a professionally accomplished alumni award from Rutgers University – Camden School of Business, and in that year he was also named an executive of the year by South Jersey Biz magazine. Hanrahan is a member of the Federal Reserve Bank of Philadelphia’s Community Depository Institutions Advisory Council. He is a director of the American Bankers Association (ABA) Foundation, is a past chairman of the ABA’s community and economic development committee, and is a past member of the ABA’s Community Bankers Council. He serves on the board of directors of Atlantic Community Bankers Bank. He also serves as a member of the Rutgers University - Camden School of Business Dean’s Leadership Council. From 2008 to 2015, he was a director and past board president of Cumberland County Habitat for Humanity. He is also a member of the Vineland Rotary Club and of Tenth Presbyterian Church in Philadelphia, Penn.

John Kandrac is a senior economist in the division of monetary affairs at the Federal Reserve Board of Governors, where he works on topics related to monetary policy implementation and money markets. His research focuses on monetary economics, banking and financial intermediation, and financial markets. Prior to joining the Federal Reserve, he was an analyst at J.P. Morgan and received his Ph.D. from the University of Oregon.

W. Blake Marsh is an economist in the Banking Research department at the Federal Reserve Bank of Kansas City. His research focuses on commercial bank regulation and financial intermediation. Current research topics examine commercial real estate lending concentrations, syndicated lending, and the adoption of financial technology. Marsh holds a bachelor’s degree in economics from The George Washington University and a Master of Arts and Ph.D.from American University. He previously held positions at the Board of Governors of the Federal Reserve System and in the mortgage industry.

W. Blake Marsh is an economist in the Banking Research department at the Federal Reserve Bank of Kansas City. His research focuses on commercial bank regulation and financial intermediation. Current research topics examine commercial real estate lending concentrations, syndicated lending, and the adoption of financial technology. Marsh holds a bachelor’s degree in economics from The George Washington University and a Master of Arts and Ph.D.from American University. He previously held positions at the Board of Governors of the Federal Reserve System and in the mortgage industry.

Andrew P. Meyer is a senior economist in the Community Bank Research and Outreach office of the Federal Reserve Bank of St. Louis. He received a doctorate in economics from Washington University in St. Louis and has worked at the Federal Reserve since 1994. In addition to his research on community banking issues, Meyer conducts statistical analysis of the downgrade and failure risk of commercial banks. He also serves on a committee to improve the Federal Reserve's off-site bank surveillance program and has taught regularly in examiner training schools.

Michelle C. Neely is an economist in the Community Bank Research and Outreach office of the Federal Reserve Bank of St. Louis. She received a master’s degree in economics from the Australian National University in Canberra, Australia, and earned undergraduate degrees in journalism, economics and policy studies from Syracuse University, Syracuse, N.Y. She has worked at the Federal Reserve for more than 20 years, with the first 10 years spent in the Research Department. In addition to research on community banking issues, she conducts analysis of regulatory and legislative issues related to the banking industry.

Andrew P. Meyer is a senior economist in the Community Bank Research and Outreach office of the Federal Reserve Bank of St. Louis. He received a doctorate in economics from Washington University in St. Louis and has worked at the Federal Reserve since 1994. In addition to his research on community banking issues, Meyer conducts statistical analysis of the downgrade and failure risk of commercial banks. He also serves on a committee to improve the Federal Reserve's off-site bank surveillance program and has taught regularly in examiner training schools.

Michelle C. Neely is an economist in the Community Bank Research and Outreach office of the Federal Reserve Bank of St. Louis. She received a master’s degree in economics from the Australian National University in Canberra, Australia, and earned undergraduate degrees in journalism, economics and policy studies from Syracuse University, Syracuse, N.Y. She has worked at the Federal Reserve for more than 20 years, with the first 10 years spent in the Research Department. In addition to research on community banking issues, she conducts analysis of regulatory and legislative issues related to the banking industry.

Allison Nicoletti joined the Wharton School of the University of Pennsylvania as an assistant professor of accounting in 2016. She holds a Ph.D. in accounting from The Ohio State University and a bachelor’s degree in accounting and economics from Illinois Wesleyan University. Prior to returning to academia, she was a senior audit associate in financial services at KPMG in Chicago, Ill., focusing on financial statement audits of bank and insurance companies and is a certified public accountant licensed in Illinois. Her research examines financial reporting and disclosure decisions made by financial institutions as well as the economic consequences of accounting standards and regulation.

Allison Nicoletti joined the Wharton School of the University of Pennsylvania as an assistant professor of accounting in 2016. She holds a Ph.D. in accounting from The Ohio State University and a bachelor’s degree in accounting and economics from Illinois Wesleyan University. Prior to returning to academia, she was a senior audit associate in financial services at KPMG in Chicago, Ill., focusing on financial statement audits of bank and insurance companies and is a certified public accountant licensed in Illinois. Her research examines financial reporting and disclosure decisions made by financial institutions as well as the economic consequences of accounting standards and regulation.

Kevin Riley is the president and chief executive officer of First Interstate BancSystem, Inc., a $12.5 billion financial holding company headquartered in Billings, Mont. Prior to his current role, he served as the bank’s chief financial officer. Prior to that, Riley served in a number of executive-level positions for several institutions, including Berkshire Hills Bancorp, a $5.3 billion financial holding company headquartered in Pittsfield, Mass., and KeyCorp, a $90 billion bank holding company headquartered in Cleveland, Ohio. Riley graduated from Northeastern University, Boston, Mass., with a Bachelor of Business Administration degree in accounting.

Kevin Riley is the president and chief executive officer of First Interstate BancSystem, Inc., a $12.5 billion financial holding company headquartered in Billings, Mont. Prior to his current role, he served as the bank’s chief financial officer. Prior to that, Riley served in a number of executive-level positions for several institutions, including Berkshire Hills Bancorp, a $5.3 billion financial holding company headquartered in Pittsfield, Mass., and KeyCorp, a $90 billion bank holding company headquartered in Cleveland, Ohio. Riley graduated from Northeastern University, Boston, Mass., with a Bachelor of Business Administration degree in accounting.

John W. Ryan is the president and CEO of the Conference of State Bank Supervisors, the national association representing state banking supervisors and the leading advocate for advancing the state banking system. Before being named CSBS president and CEO in August 2011, Ryan was CSBS's executive vice president, a position he had held since October 2003. He first joined CSBS in 1997 as an assistant vice president for legislative affairs. Prior to joining CSBS, Ryan worked at Newmyer Associates, a public affairs consulting firm, where he led the company's financial services consulting practice. Previous to his work at Newmyer Associates, Ryan spent four years as a professional staff member to the U.S. House of Representatives Committee on Banking, Finance and Urban Affairs. Ryan received a bachelor's degree in political science and economics from the University of California-Berkeley.

Peter F. Schork is the president and chief executive officer of Ann Arbor State Bank, Ann Arbor, Mich. Ann Arbor State Bank received its FDIC insurance approval in November 2008 and opened in January 2009. From 2005 to 2008, Schork was vice president of Edward Surovell Realtors; he also co-founded Surovell Financial (mortgage) Company and Surovell Settlement and Title Services Agency. From 1998 to 2005, he served as first president of personal banking, retail branches and mortgage lending at the Bank of Ann Arbor. He also served as the bank’s Community Reinvestment Act officer. From 1982 to 1998, he served in progressively more advanced positions in private banking, lending, branch management, and mortgage lending with Key Bank. Schork is active in many local non-profit boards in the Ann Arbor and Ypsilanti areas. He holds a Master of Business Administration degree in finance from Eastern Michigan University, and a bachelor’s degree in economics and political science from the University of Michigan.

Peter F. Schork is the president and chief executive officer of Ann Arbor State Bank, Ann Arbor, Mich. Ann Arbor State Bank received its FDIC insurance approval in November 2008 and opened in January 2009. From 2005 to 2008, Schork was vice president of Edward Surovell Realtors; he also co-founded Surovell Financial (mortgage) Company and Surovell Settlement and Title Services Agency. From 1998 to 2005, he served as first president of personal banking, retail branches and mortgage lending at the Bank of Ann Arbor. He also served as the bank’s Community Reinvestment Act officer. From 1982 to 1998, he served in progressively more advanced positions in private banking, lending, branch management, and mortgage lending with Key Bank. Schork is active in many local non-profit boards in the Ann Arbor and Ypsilanti areas. He holds a Master of Business Administration degree in finance from Eastern Michigan University, and a bachelor’s degree in economics and political science from the University of Michigan.

Julie Stackhouse is executive vice president and managing officer of supervision, credit, community development and learning innovation for the Federal Reserve Bank of St. Louis. Prior to joining the St. Louis Fed in September 2002, Stackhouse served as vice president and managing officer of the Risk Management department of the Federal Reserve Bank of Minneapolis. In addition, she was formerly an officer with the Federal Reserve Bank of Kansas City prior to relocating to Minnesota in 1995. She served in many capacities at the Kansas City Reserve Bank, starting as an examiner in 1980. Stackhouse holds a bachelor's degree in business administration from Drake University and is a graduate of the Wisconsin Graduate School of Banking. She currently serves as president-elect of the Board for National Charity League, Inc., a mother-daughter philanthropic organization, and as a member of the St. Louis Forum. In 2010, Stackhouse was named a St. Louis Business Journal “Most Influential Business Women” recipient, and in 2016, was recognized with the Delta Sigma Pi Lifetime Achievement Award.

Michael Stevens is the senior executive vice president at the Conference of State Bank Supervisors (CSBS). He is responsible for leading the organization's public policy, financial supervision, federal coordination, communications, industry relations and professional development functions. Stevens also serves as the principal deputy to the state banking member of the Financial Stability Oversight Council. Prior to his appointment in September 2011, he served as the senior vice president for regulatory policy, representing the state banking system in the development of policy in the areas of financial stability, prudential supervision and consumer protection. He joined CSBS in 1999 to work in all facets of CSBS's professional development division. Stevens is a frequent instructor and speaker on banking policy, examinations and financial analysis. He serves on the faculty of the Graduate School of Banking at Colorado and at Texas Tech University's School of Banking. He began his regulatory career as a bank examiner for the Iowa Division of Banking, where he served 11 years.

Steven W. Streit is founder and chief executive officer of Pasadena-based Green Dot Corporation (NYSE: GDOT) and founder and chairman of its wholly owned subsidiary bank, Green Dot Bank. Green Dot, founded in 1999, is a technology-focused bank holding company with a mission to reinvent banking for the masses. Streit has led Green Dot to become both the largest provider of reloadable prepaid debit cards and cash reload processing services in the U.S. and a leader in mobile banking and financial technology. He has been recognized for numerous industry awards over the years, including being a two-time winner of EY Entrepreneur Of The Year, and was recently appointed by the Federal Reserve Bank of San Francisco to serve on its Los Angeles Branch board of directors. Streit is also a philanthropist, focusing his efforts on single mothers with young children through the family charity named after his mother, Patti’s Way. In addition to his business success, has been recognized as a humanitarian and philanthropist through many awards and honors over the years.

Steven W. Streit is founder and chief executive officer of Pasadena-based Green Dot Corporation (NYSE: GDOT) and founder and chairman of its wholly owned subsidiary bank, Green Dot Bank. Green Dot, founded in 1999, is a technology-focused bank holding company with a mission to reinvent banking for the masses. Streit has led Green Dot to become both the largest provider of reloadable prepaid debit cards and cash reload processing services in the U.S. and a leader in mobile banking and financial technology. He has been recognized for numerous industry awards over the years, including being a two-time winner of EY Entrepreneur Of The Year, and was recently appointed by the Federal Reserve Bank of San Francisco to serve on its Los Angeles Branch board of directors. Streit is also a philanthropist, focusing his efforts on single mothers with young children through the family charity named after his mother, Patti’s Way. In addition to his business success, has been recognized as a humanitarian and philanthropist through many awards and honors over the years.

John C. Williams took office as president and chief executive officer of the Federal Reserve Bank of San Francisco on March 1, 2011. In this role, he serves on the Federal Open Market Committee, bringing the Federal Reserve’s Twelfth District’s perspective to monetary policy discussions in Washington. Williams was previously the executive vice president and director of research for the San Francisco bank, which he joined in 2002. He began his career in 1994 as an economist at the Board of Governors of the Federal Reserve System, following the completion of his Ph.D. in economics at Stanford University. Prior to that, he earned a Master of Science from the London School of Economics, and an A.B. from the University of California at Berkeley. Williams’ research focuses on topics including: monetary policy under uncertainty; innovation; and business cycles. Additionally, he served as senior economist at the White House Council of Economic Advisers and as a lecturer at Stanford University’s Graduate School of Business.

John C. Williams took office as president and chief executive officer of the Federal Reserve Bank of San Francisco on March 1, 2011. In this role, he serves on the Federal Open Market Committee, bringing the Federal Reserve’s Twelfth District’s perspective to monetary policy discussions in Washington. Williams was previously the executive vice president and director of research for the San Francisco bank, which he joined in 2002. He began his career in 1994 as an economist at the Board of Governors of the Federal Reserve System, following the completion of his Ph.D. in economics at Stanford University. Prior to that, he earned a Master of Science from the London School of Economics, and an A.B. from the University of California at Berkeley. Williams’ research focuses on topics including: monetary policy under uncertainty; innovation; and business cycles. Additionally, he served as senior economist at the White House Council of Economic Advisers and as a lecturer at Stanford University’s Graduate School of Business.

Timothy Yeager is professor of finance and holds the Arkansas Bankers Association Chair in Banking at the University of Arkansas. His responsibilities include teaching, research, and outreach to Arkansas bankers. Prior to joining the University in January 2006, Yeager was an assistant vice president in the Federal Reserve Bank of St. Louis’ supervision division. His articles have been published in journals such as the Journal of Financial Intermediation, Journal of Money Credit and Banking, Journal of Financial Stability, and the Journal of Banking and Finance. He has been quoted in numerous state and national news outlets and his work has been featured in national newspapers and select trade publications. Tim received his Ph.D. in Economics in 1993 from Washington University in St. Louis.

Timothy Yeager is professor of finance and holds the Arkansas Bankers Association Chair in Banking at the University of Arkansas. His responsibilities include teaching, research, and outreach to Arkansas bankers. Prior to joining the University in January 2006, Yeager was an assistant vice president in the Federal Reserve Bank of St. Louis’ supervision division. His articles have been published in journals such as the Journal of Financial Intermediation, Journal of Money Credit and Banking, Journal of Financial Stability, and the Journal of Banking and Finance. He has been quoted in numerous state and national news outlets and his work has been featured in national newspapers and select trade publications. Tim received his Ph.D. in Economics in 1993 from Washington University in St. Louis.

Janet L. Yellen took office as chair of the Board of Governors of the Federal Reserve System on February 3, 2014, for a four-year term ending February 3, 2018. Yellen also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Prior to her appointment as Chair, Yellen served as vice chair of the Board of Governors, taking office in October 2010, when she simultaneously began a 14-year term as a member of the Board that will expire January 31, 2024. Yellen is Professor Emeritus at the University of California at Berkeley where she was the Eugene E. and Catherine M. Trefethen Professor of Business and Professor of Economics and has been a faculty member since 1980. She took leave from Berkeley for five years starting August 1994. She served as a member of the Board of Governors of the Federal Reserve System through February 1997, and then left the Federal Reserve to become chair of the Council of Economic Advisers through August 1999. She also chaired the Economic Policy Committee of the Organization for Economic Cooperation and Development from 1997 to 1999. She also served as president and chief executive officer of the Federal Reserve Bank of San Francisco from 2004 to 2010. She is a member of both the Council on Foreign Relations and the American Academy of Arts and Sciences. She has served as president of the Western Economic Association, vice president of the American Economic Association and a fellow of the Yale Corporation. She graduated summa cum laude from Brown University with a degree in economics in 1967, and received her Ph.D. in Economics from Yale University in 1971. She received the Wilbur Cross Medal from Yale in 1997, an honorary doctor of laws degree from Brown in 1998, and an honorary doctor of humane letters from Bard College in 2000. An Assistant Professor at Harvard University from 1971 to 1976, Yellen served as an Economist with the Federal Reserve's Board of Governors in 1977 and 1978, and on the faculty of the London School of Economics and Political Science from 1978 to 1980. Yellen has written on a wide variety of macroeconomic issues, while specializing in the causes, mechanisms, and implications of unemployment.

Janet L. Yellen took office as chair of the Board of Governors of the Federal Reserve System on February 3, 2014, for a four-year term ending February 3, 2018. Yellen also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Prior to her appointment as Chair, Yellen served as vice chair of the Board of Governors, taking office in October 2010, when she simultaneously began a 14-year term as a member of the Board that will expire January 31, 2024. Yellen is Professor Emeritus at the University of California at Berkeley where she was the Eugene E. and Catherine M. Trefethen Professor of Business and Professor of Economics and has been a faculty member since 1980. She took leave from Berkeley for five years starting August 1994. She served as a member of the Board of Governors of the Federal Reserve System through February 1997, and then left the Federal Reserve to become chair of the Council of Economic Advisers through August 1999. She also chaired the Economic Policy Committee of the Organization for Economic Cooperation and Development from 1997 to 1999. She also served as president and chief executive officer of the Federal Reserve Bank of San Francisco from 2004 to 2010. She is a member of both the Council on Foreign Relations and the American Academy of Arts and Sciences. She has served as president of the Western Economic Association, vice president of the American Economic Association and a fellow of the Yale Corporation. She graduated summa cum laude from Brown University with a degree in economics in 1967, and received her Ph.D. in Economics from Yale University in 1971. She received the Wilbur Cross Medal from Yale in 1997, an honorary doctor of laws degree from Brown in 1998, and an honorary doctor of humane letters from Bard College in 2000. An Assistant Professor at Harvard University from 1971 to 1976, Yellen served as an Economist with the Federal Reserve's Board of Governors in 1977 and 1978, and on the faculty of the London School of Economics and Political Science from 1978 to 1980. Yellen has written on a wide variety of macroeconomic issues, while specializing in the causes, mechanisms, and implications of unemployment.

Video Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}